Evolving Neo Financial

How good design helped turn a simple fintech product into a full ecosystem ready to take on the big five banks.

Info. Architecture

UX Strategy

Design System

Sorry, this case study requires a desktop browser 1200px or wider.

Back

the problem

October 2023

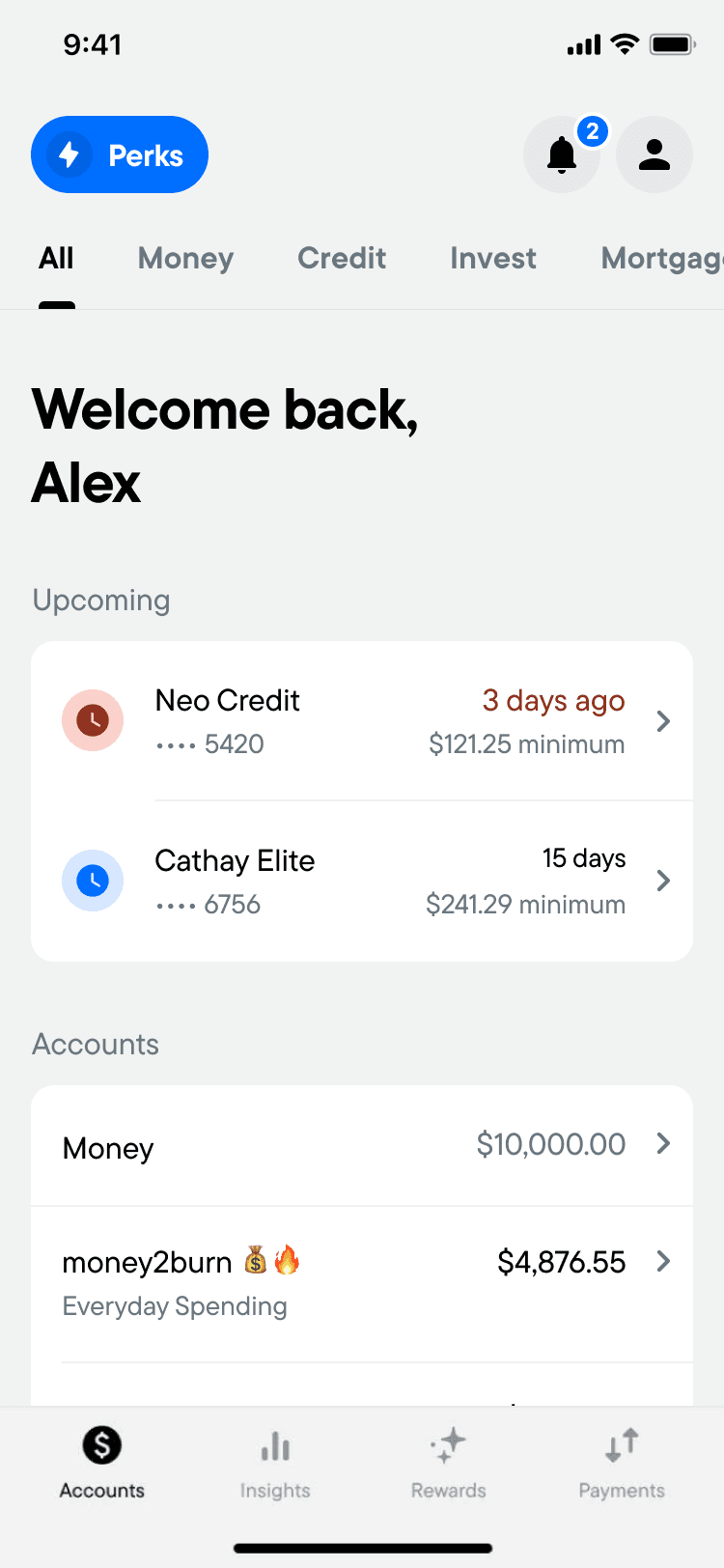

Neo's business is evolving faster than the app

The product lineup was growing fast, starting to look more like a big bank. The app’s foundation had to evolve to keep up with this next phase of growth.

New products are breaking the information architecture

“Money” was the first account to grow into a full category of accounts. It marked a key shift: a mini-ecosystem starting to form inside a single-product architecture. This added a new layer of complexity to what used to be a simple experience, and it started to break down the way customers thought about the app.

With even more product categories on the horizon, the architecture would need to evolve to support them properly.

New account features aren't finding a proper home

Each of our products has a unique and growing feature set. Some of these features are critical to both customers and the business. Without a design evolution, important features are ending up buried in submenus.

As we scale our accounts to match the market, we’ll need to thoughtfully design these features into the core experience to encourage engagement.

February 2024

the strategy

Evolving the information architecture

We needed to expand the information architecture to give customers a clearer way to navigate their accounts, perform tasks, and manage their financial goals.

Introducing a category layer

As mentioned, each category of accounts is like a mini ecosystem of its own — a small world that solves a specific financial goal. To support these new surface areas, we needed a new layer of architecture. We needed to give customers room to unpack a larger mental model:

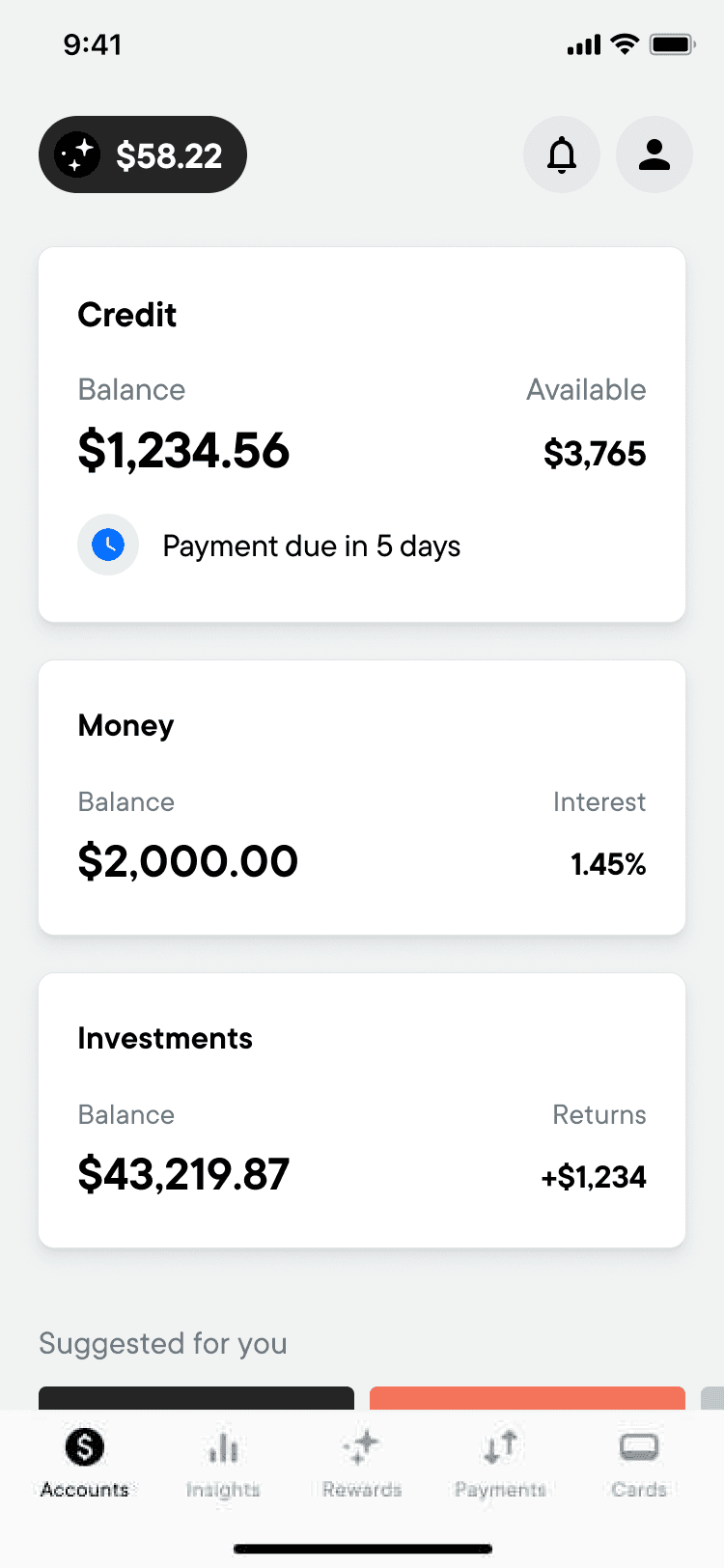

A first layer that captures their overall financial situation

A second layer that focuses on a specific financial category

A third layer for each individual account, where customers can dive deep into management

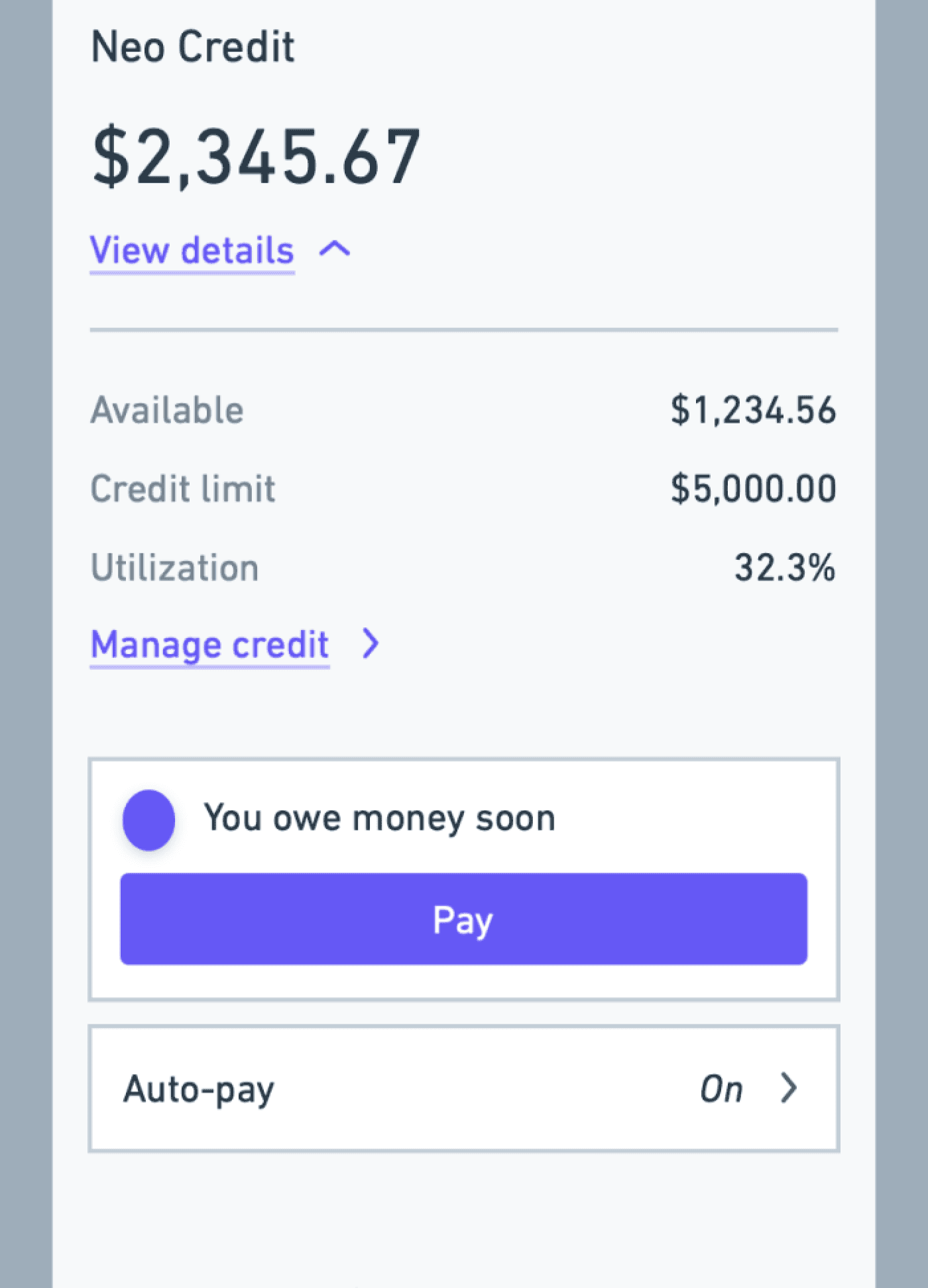

Neo Credit

HBC

Credit

Neo World Elite

Cathay World Elite

Neo Secured Credit

CREDIT

Everyday Spending

High-interest Savings

GIC

MONEY

Managed Investing

Self-directed trading

Crypto

INVEST

Line of Credit

Instalment plans

Personal loans

LOANS

New

Re-mortgage

Re-finance

MORT.

Home

Auto

Tenant

INSURE

Accounts

The foundation of each account.

Categories

A group representing products of the same type.

Home/All

The entry point of the account experience.

A customer-first system framework

Stepping back from the accounts themselves let us focus on what matters most to customers. Across all accounts, we could see which information and actions made it easier for people to understand their accounts and take quick action.

Designing around these insights helped us stay focused on customer goals, even as the system grew more complex. It also gave us patterns that worked across the whole product line, so no matter what account a customer used, the experience always felt familiar and easy to navigate.

Balance

Spend

Interest rate

Balance

Goal progress

Interest rate

Earned to date

Balance

Realization

Interest rate

Earned to date

Balance

Available

Statement balance

Balance

Available

Statement balance

Balance

Available

Balance

Return %

Earnings

Balance

Return %

Earnings

Watchlist

Balance

Return %

Earnings

Watchlist

Deposit

Transfer

Withdraw

Deposit

Transfer

Withdraw

Auto-Save

Pay balance

Pay balance

Pay balance

Deposit

Auto-Invest

Search

Buy

Deposit

Sell

Search

Buy

Deposit

Sell

Activate card

View card details

Auto-Save

Edit goal

Manage credit limit

View statements

Auto-Pay

Manage credit limit

View statements

Auto-Pay

Manage security fund

Withdraw

Edit goal

Change risk profile

Balance

Goal progress

Interest rate

Earned to date

Balance

Realization

Interest rate

Earned to date

Edit name

View DD details

View statements

View T5 Slips

View agreements

Close account

Edit name

View statements

View T5 Slips

View agreements

Close account

Edit name

View T5 Slips

View agreements

Close account

Balance

Spend

Interest rate

Balance

Goal progress

Interest rate

Earned to date

Balance

Realization

Interest rate

Earned to date

View statements

View tax forms

View agreements

Close account

View statements

View tax forms

View agreements

Close account

View statements

View tax forms

View agreements

Close account

Purchases

Transfers

Predictive deposits

Transfers

Predicted goal end date

Initial deposit

Realization date

Purchases

Subscription

Purchases

Subscription

Purchases

Credit impact

Dividends

Buys

Sells

Dividends

Buys

Sells

Duplicate charges

Declined transactions

Card expiring

KYC review approaching

Balance

Goal progress

Interest rate

Earned to date

Balance

Realization

Interest rate

Earned to date

Overdue payment

Duplicate charges

Declined transactions

Card expiring

KYC review approaching

Overdue payment

Duplicate charges

Declined transactions

Card expiring

KYC review approaching

Duplicate charges

Declined transactions

Card expiring

KYC review approaching

Annual assessment due

Balance near minimum

Annual assessment due

Fraud detected

Overdue KYC lock

Closed

Overdue KYC lock

Closed

Overdue KYC lock

Closed

Delinquent

Fraud detected

Overdue KYC lock

Closed

Delinquent

Fraud detected

Overdue KYC lock

Closed

Fraud detected

Overdue KYC lock

Closed

Overdue KYC lock

Insufficient funds

Closed

Overdue KYC lock

Closed

Overdue KYC lock

Closed

Key performance indicators

Primary actions

Secondary actions

Uncommon actions

Upcoming & Historical

Warning states

Critical states

Money

Everyday

HISA

GIC

Credit

Standard

World

Secured

Invest

Managed

Self-directed

Crypto

System patterns

Redesigning accounts with context

The word “context” comes from Latin and means “to weave together." It gives meaning to information and events. By putting customers’ financial data in context, we can help them understand their own story and take action more easily.

Creating contextual groupings

Before getting into wireframes, we focused on how to present information in a more meaningful way. In a data-heavy environment, keeping things in context makes it easier for customers to find their way.

This approach makes sure the systems and relationships we’re building will fit naturally into the upcoming redesign.

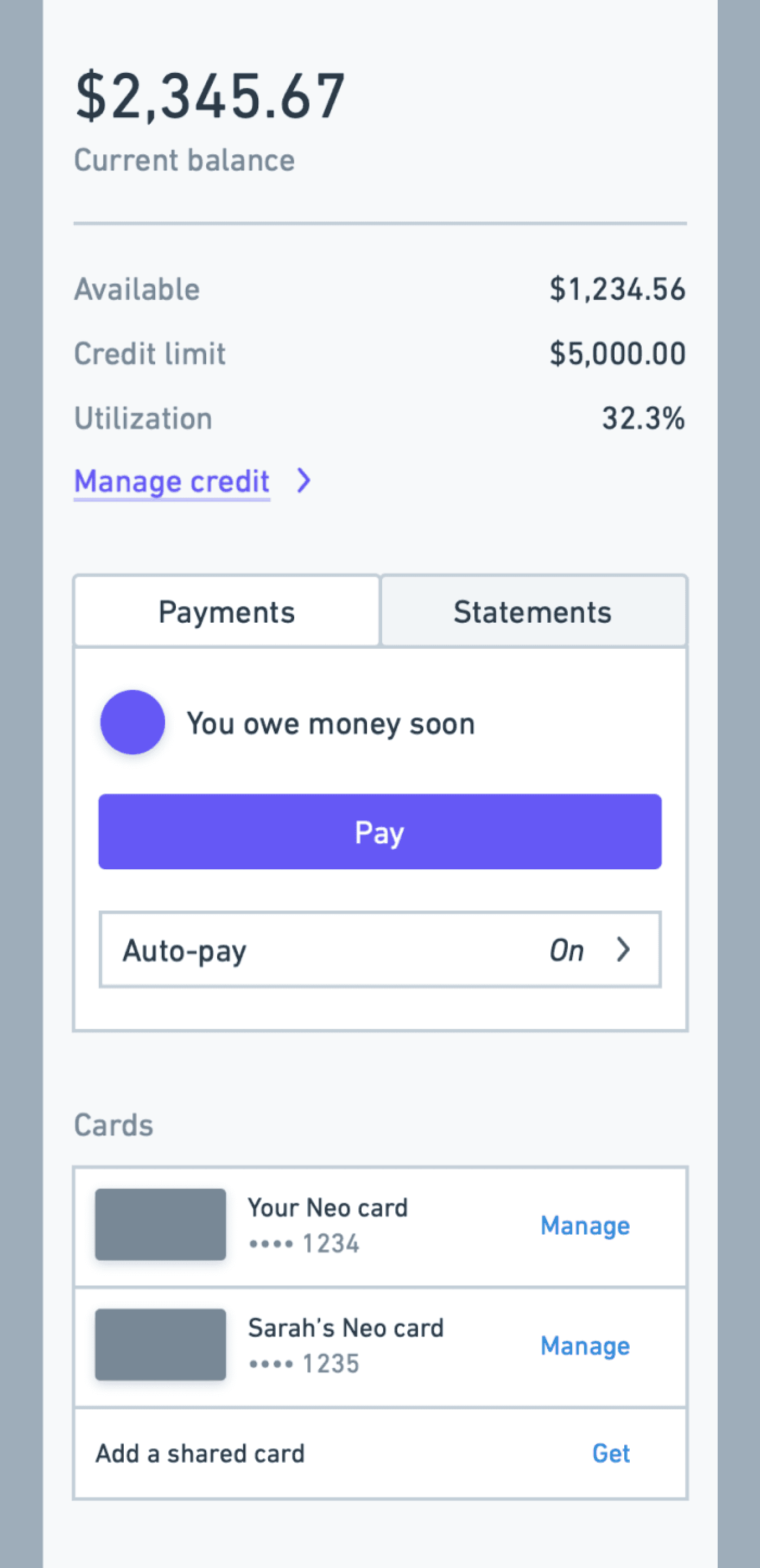

Current balance

Pending total

Posted total

Balance protection

Overlimit protection

Available credit

Credit limit

Credit Utilization %

Request Limit Increase

Reallocate credit (multi)

Payment notice

Pay flow

Auto-pay

Statements

Hardship solutions

Main card

Add card to wallet

Shared cards

Add new card

Pending transactions

Posted transactions

Account number

Agreements

Close account

Total balance

Available balance

On hold

Pending total

Overdraft protection

Monthly spend

Trends

Save w/ HISA

Add funds

Move funds

Auto-save

Statements

Main card

Add card to wallet

Shared cards

Add new card

Pending transactions

Posted transactions

Account number

Direct deposit details

Edit account name

T5 Slips

Agreements

Close account

Total balance

On hold

Goal progress

Interest rate

Lifetime earned

Convert to GIC

Add funds

Move funds

Auto-save

Statements

Posted transactions

Account number

Direct deposit details

Edit account name

T5 Slips

Agreements

Close account

Total balance

On hold

Term progress

Principal

Estimated final balance

Interest rate

Term end date

Initial deposits

Account number

Edit account name

T5 Slips

Agreements

Close account

Credit

Everyday Spending

High–interest Savings

GIC

Balances

Health

Move Money

Cards

Transactions

Details

Account type

Translating it to screens and layout

With the contextual groups defined, we explored how they could come to life in the interface.

These four lo-fi concepts show different ways to organize information by keeping related content together, highlighting key actions, and making navigation feel more natural.

Each concept on the right builds directly on the principles we set in the last step.

Infinite scroll

Recent Trx

Mid-page tabs

Full page tabs

Retain the infinite scroll

We retain the infinite scroll transaction list and establish a hierarchy vertically on the page.

Development cost

$

$

$

Scalability

Experience

Why this concept?

I feel that when redesigning or adding to an experience, it’s helpful to explore the path of least resistance. It’s not often the best solution, but it can help to highlight the issues with the design and validate the need for a more robust solution.

Recent transactions card

We show a shortlist of recent transactions and move the full scroll transaction list to a dedicated child page.

Development cost

$

$

$

Scalability

Experience

Why this concept?

A number of our transactions use cases are tied to recency, for example, checking for payroll deposits or confirming the last transaction. This approach maintains this ‘quick glance’ ability while offering more flexibility ranking the card in the hierarchy.

Mid-page tabbed sections

We keep a core content section at the top of the page while introducing a tabbed page menu below.

Development cost

$

$

$

Scalability

Experience

Why this concept?

It allows us to keep the current infinite scroll transaction list while positioning less common but important actions nearby. It’s likely to be the least disruptive change as customers start to operate in a more complex page.

Full-page tabbed sections

We introduce a tabbed menu at the top of the page and and keep a core content section in the top ranked tab.

Development cost

$

$

$

Scalability

Experience

Why this concept?

If the mid-page tab menu creates clear primary and secondary content areas, this concept goes a step further to ask what if each content area was to be presented more equally in the architecture.

the examples

Evolving the payments mental model

Managing a single credit card payment is simple. Managing multiple payments each month gets complex quickly.

The credit payment flow benefited from its position in the single-product architecture

The Credit tile sat at the top of the home page, with a dynamic payment notice counting down to the due date. Customers could simply open the app to stay informed.

But that would break in a multi-product world

As we tried to scale this design, the things that mattered most to customers quickly got lost in a busy page. With more lending accounts in play, the design lost its ability to manage payment anxiety.

It showed how important it was to move away from a siloed account model and focus on building systems around these key use cases.

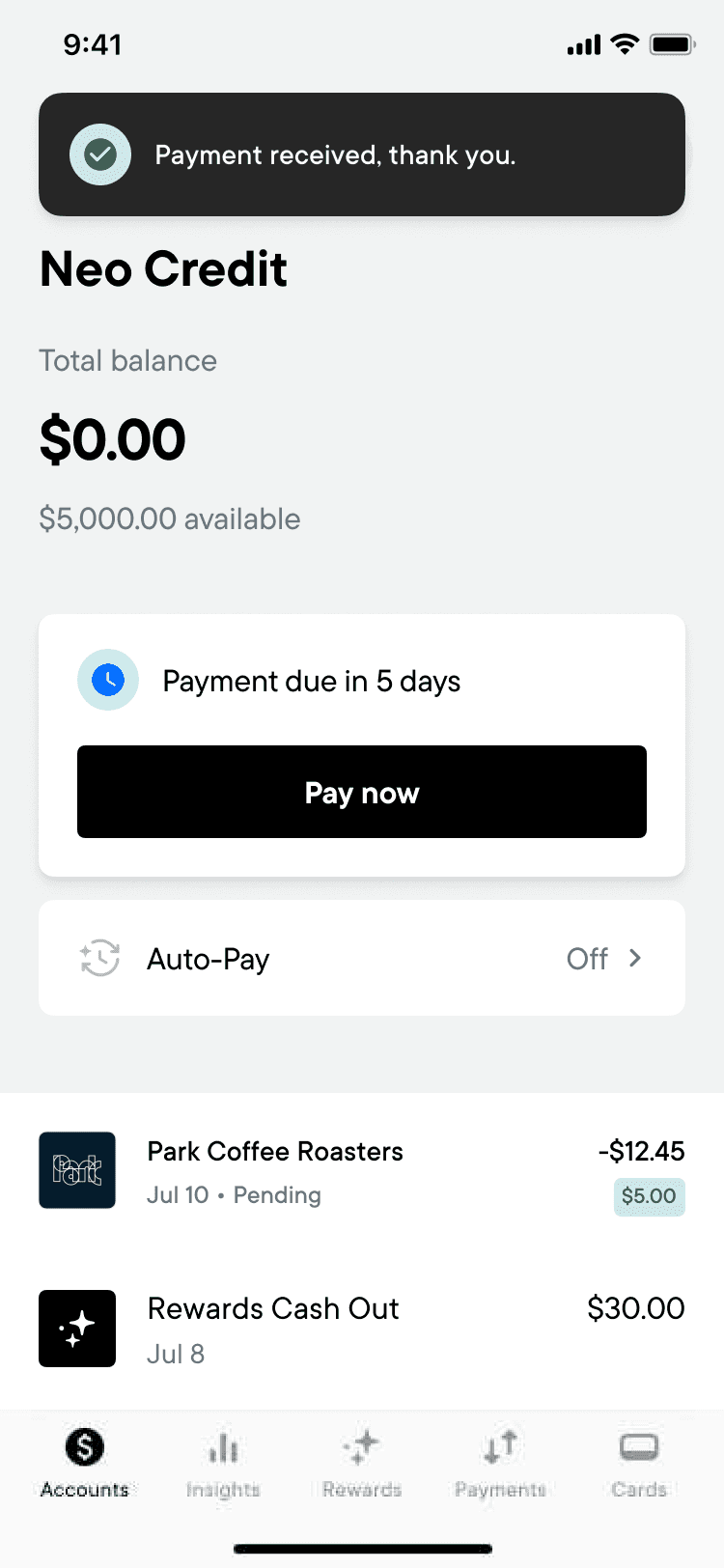

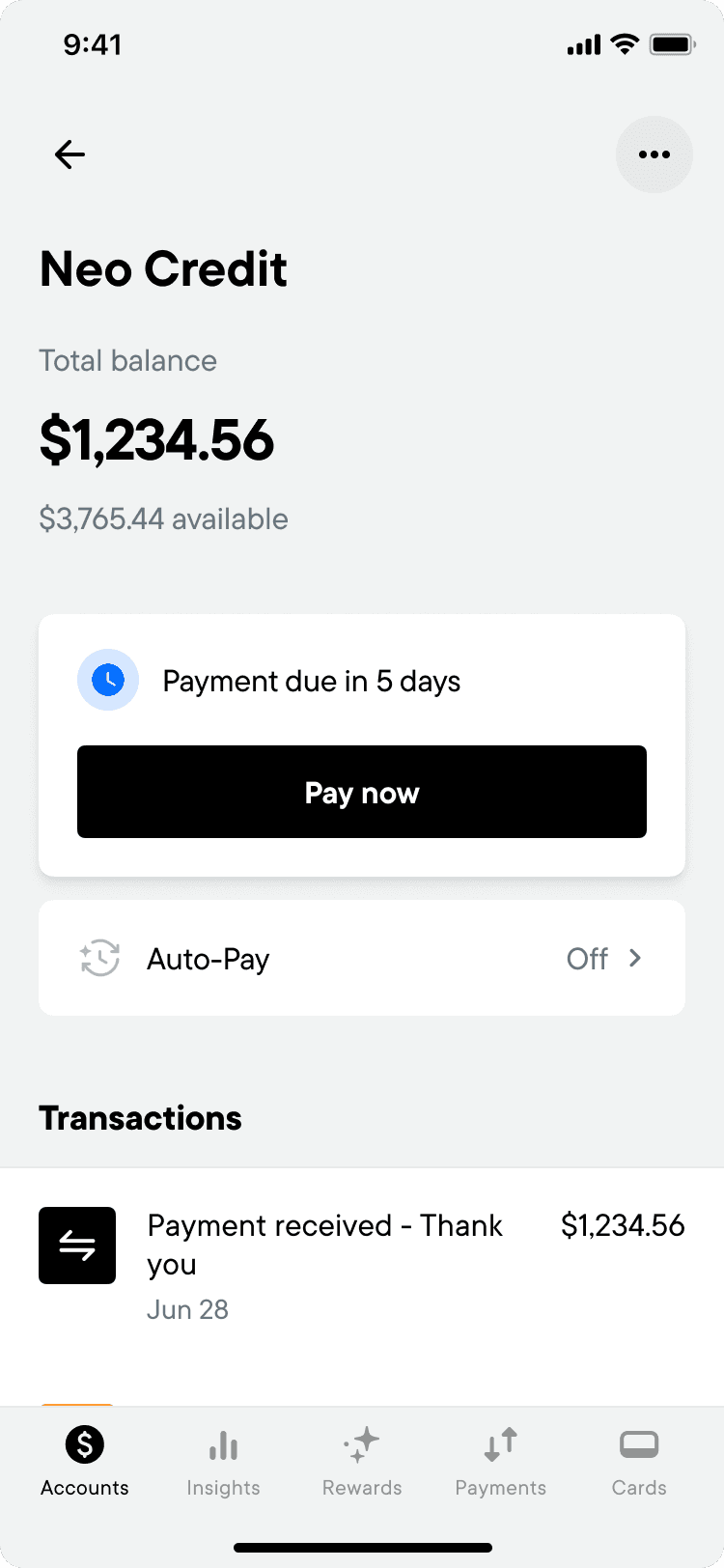

Reducing payment complexity with a system approach

By stepping back from individual accounts and focusing on repayment at a system level, we could build around what matters most to customers: the amount due and the due date.

This gave us the flexibility to design a UI that matches how people actually think — in this case, a simple list of upcoming payments that mirrors how they experience time.

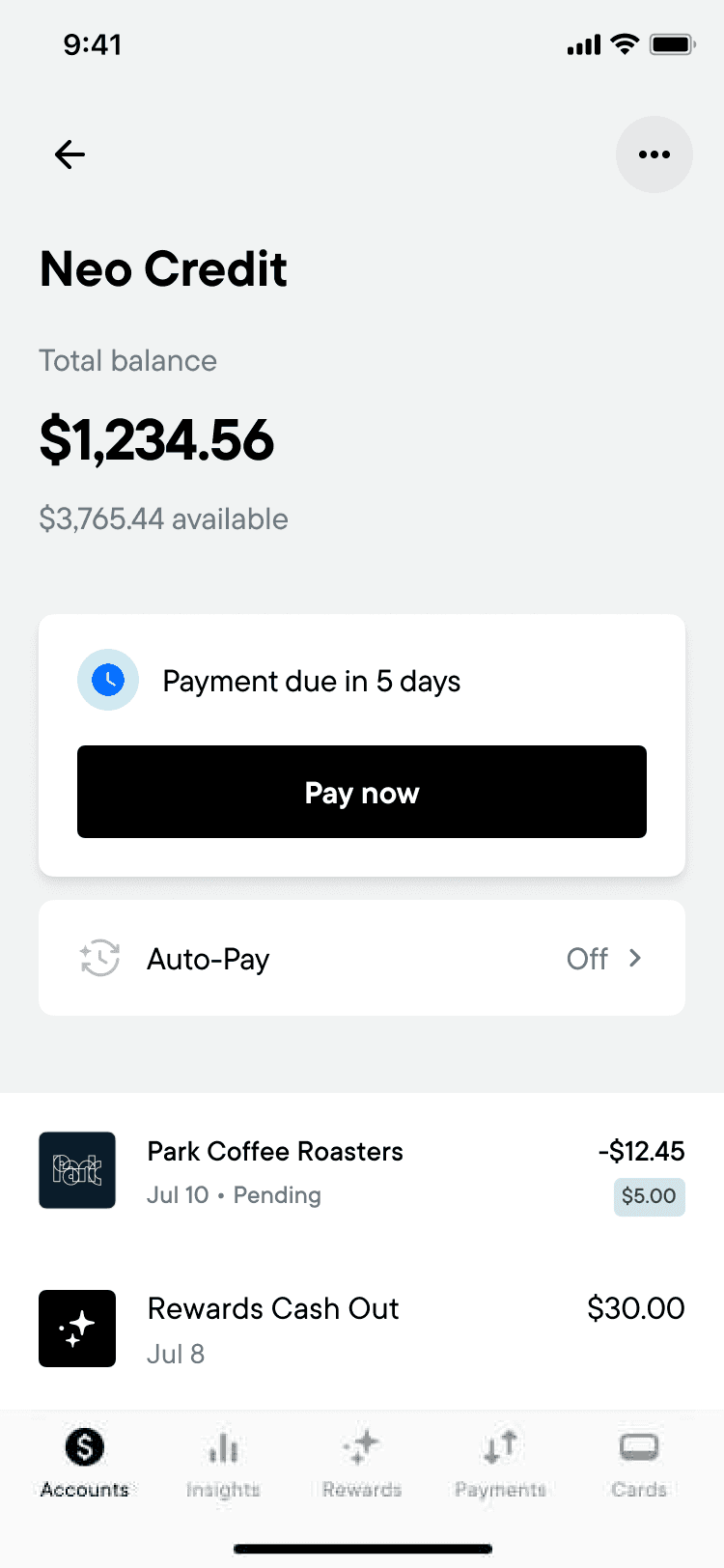

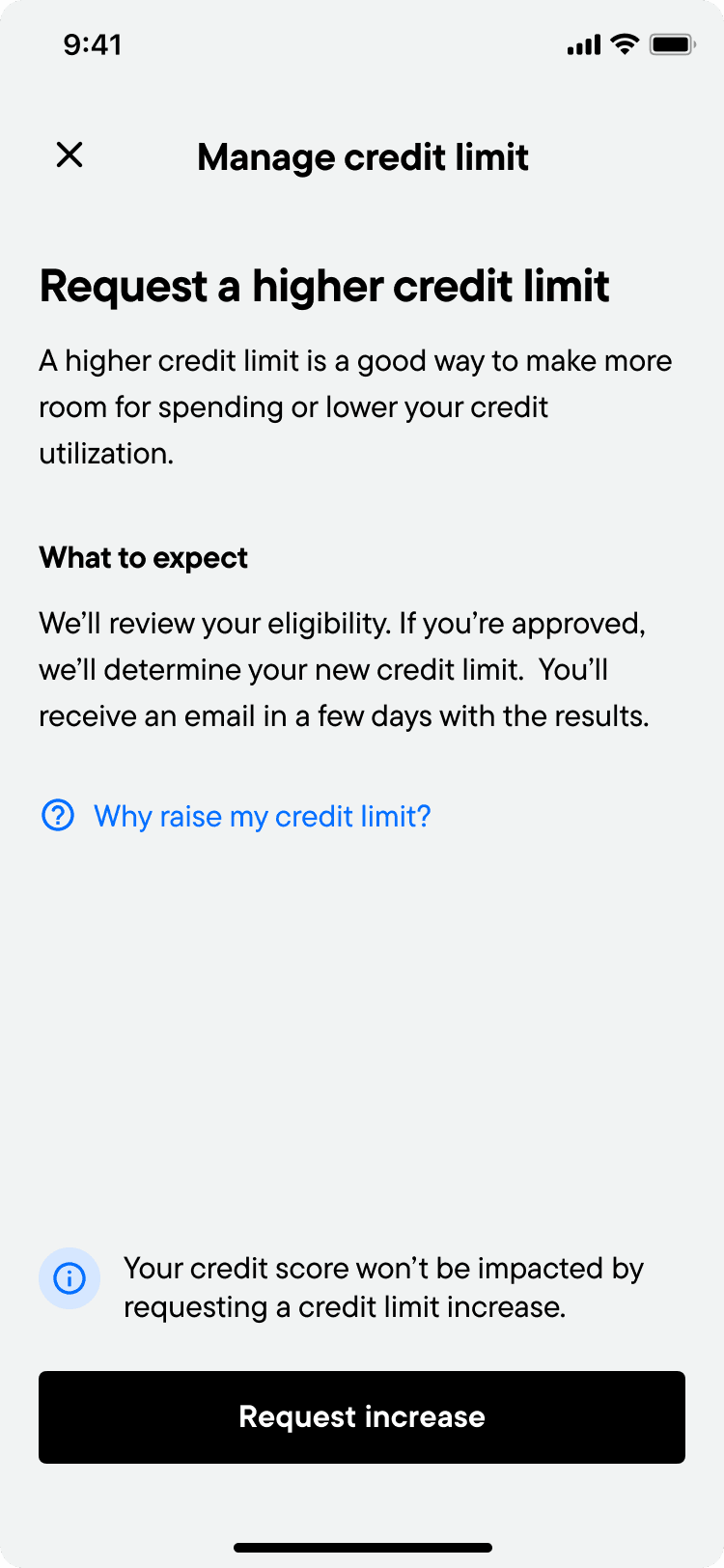

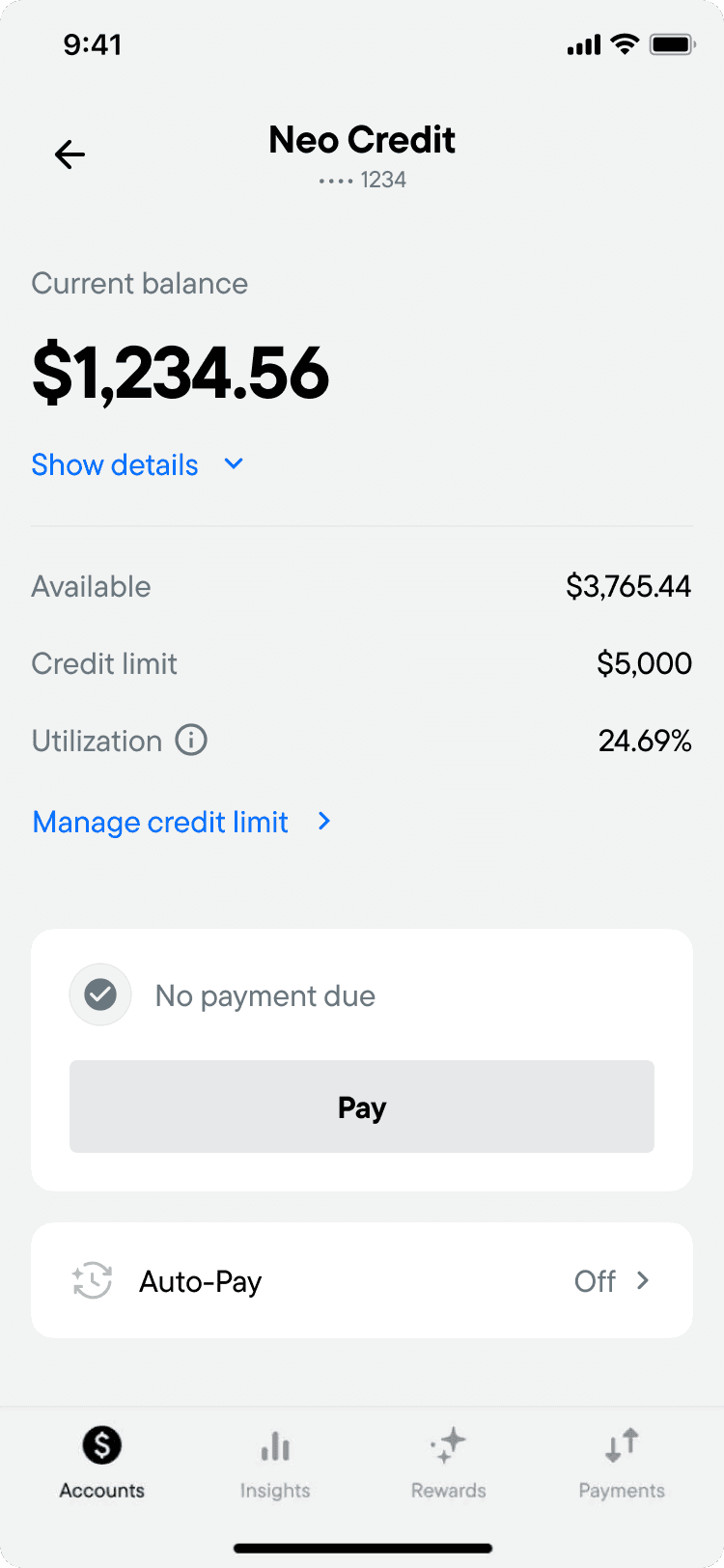

Raising credit limit awareness

Bringing credit utilization into the core story of a credit account drove a lasting increase in engagement.

Credit limit management was hidden and disconnected

The feature was launched quickly and ended up disconnected from key information. Even customers who had already decided to change their credit limit had to hunt for it, because it wasn’t placed in the right context inside the app.

Making account health visible and actionable

Technically, the change was simple. Using our context framework, we grouped a few metrics and an action, and moved them closer to the surface.

But the substance of the change was significant. Customers could now keep the health of their accounts front of mind. It also opened the door for more tailored messaging that could be acted on immediately.

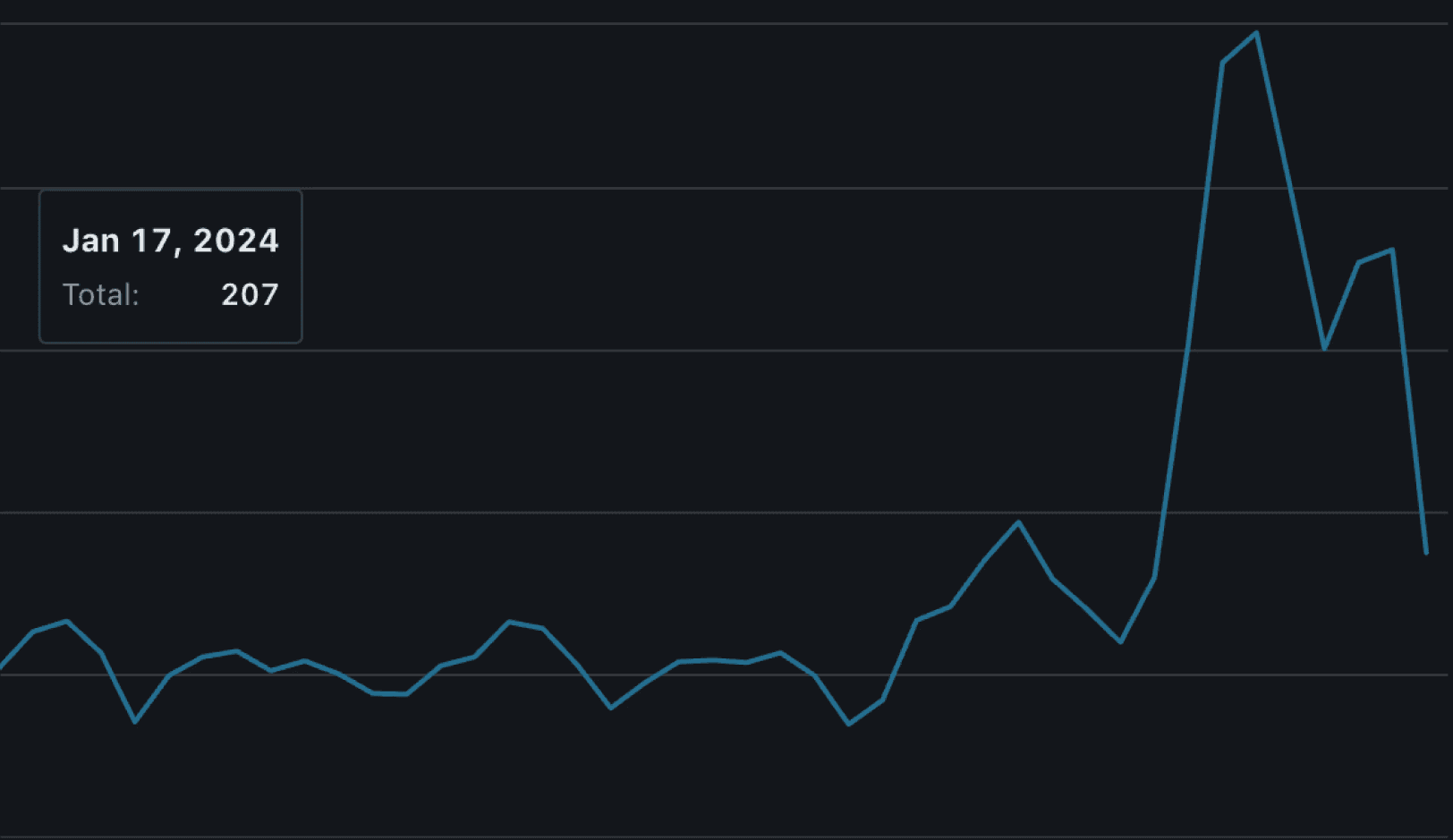

Requests for more credit increase 500%

Our week-over-week analysis showed that credit limit increase requests doubled after launch, and eventually climbed to five times the old rate once the updates were fully live.

It was an early sign that putting customer data in context could drive a real jump in engagement. It also helped build the momentum we needed to get stakeholder buy-in for the full redesign of our account pages.

Requests for more credit (WoW)

App

launch

Web

launch

App

Launch

Web

the updates

Building a system that could scale

What we were building needed to scale into an uncertain future and support products we hadn't dreamt of yet. To ensure these patterns and principles could continue to evolve, we had to clearly share our design philosophy with the wider team.

Defining page-level design principles

Each page was structured to reflect the in-context groupings we set out to create. We needed to clearly define and explain these page principles so future designers could stay aligned and build on them.

For example, every account details page follows a common template shaped by these principles, making it easier for others to keep scaling the app as products are added and evolve.

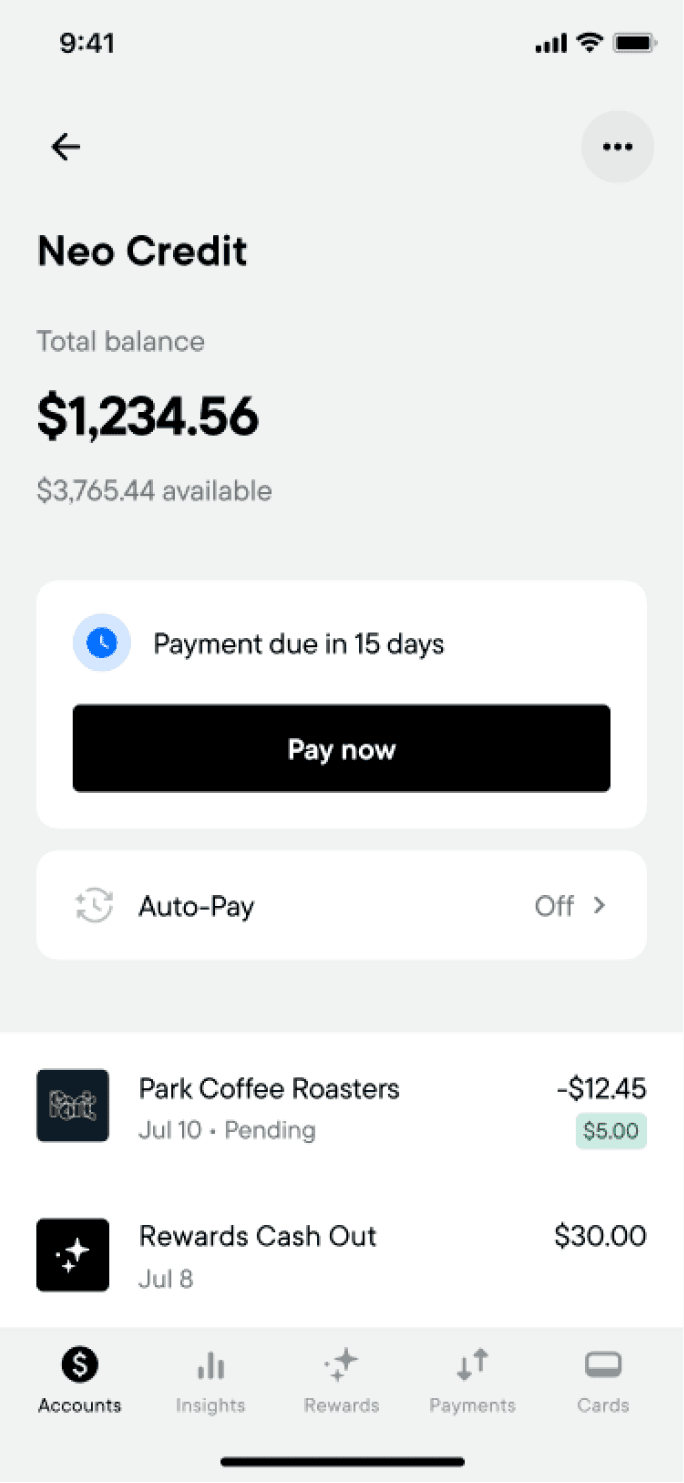

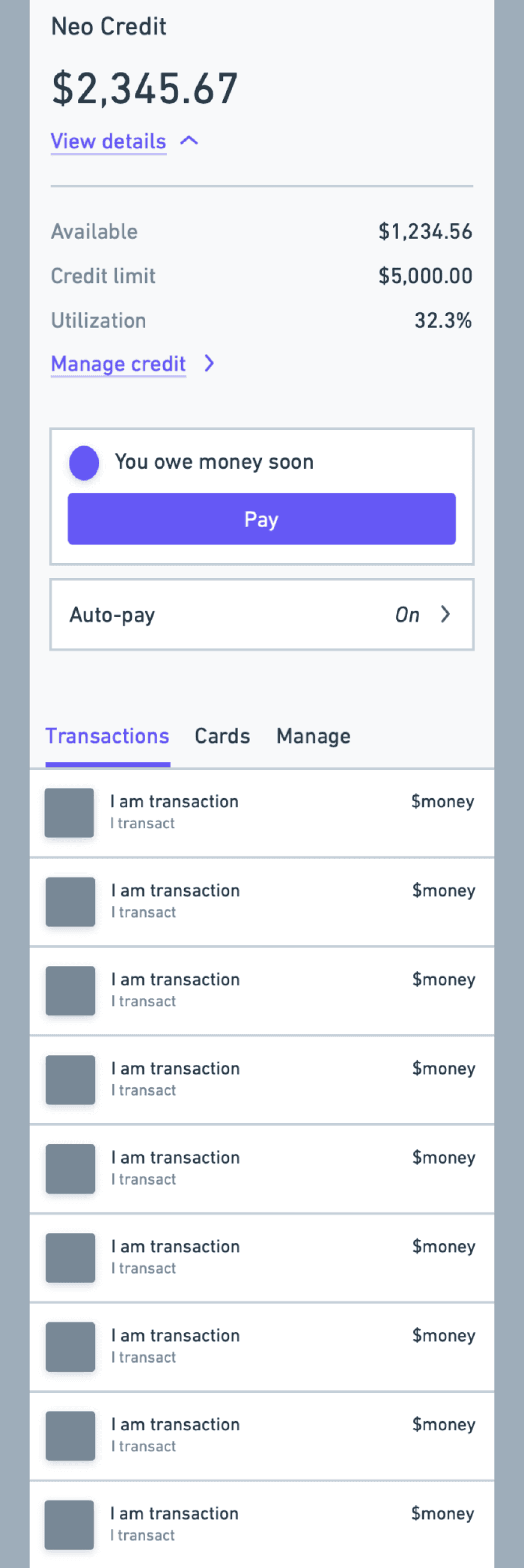

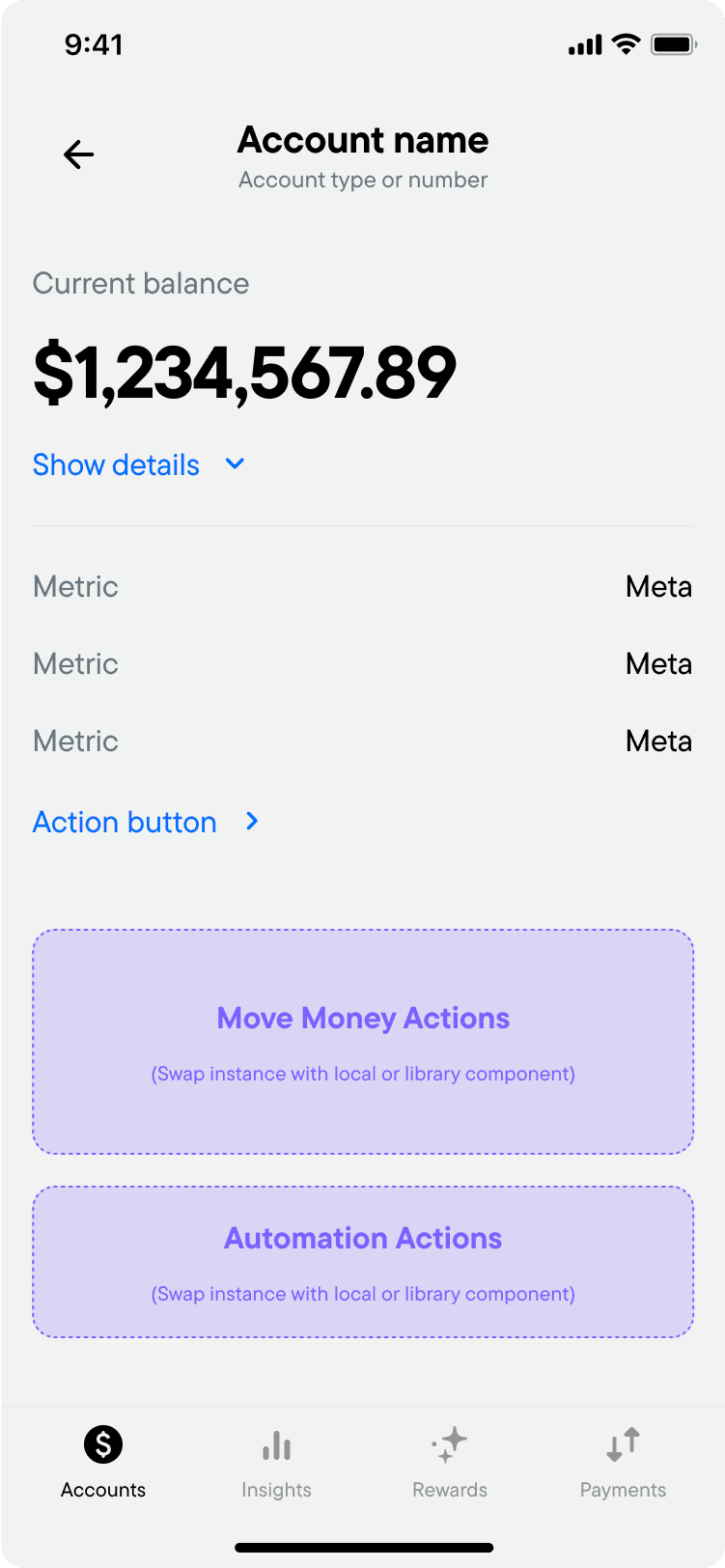

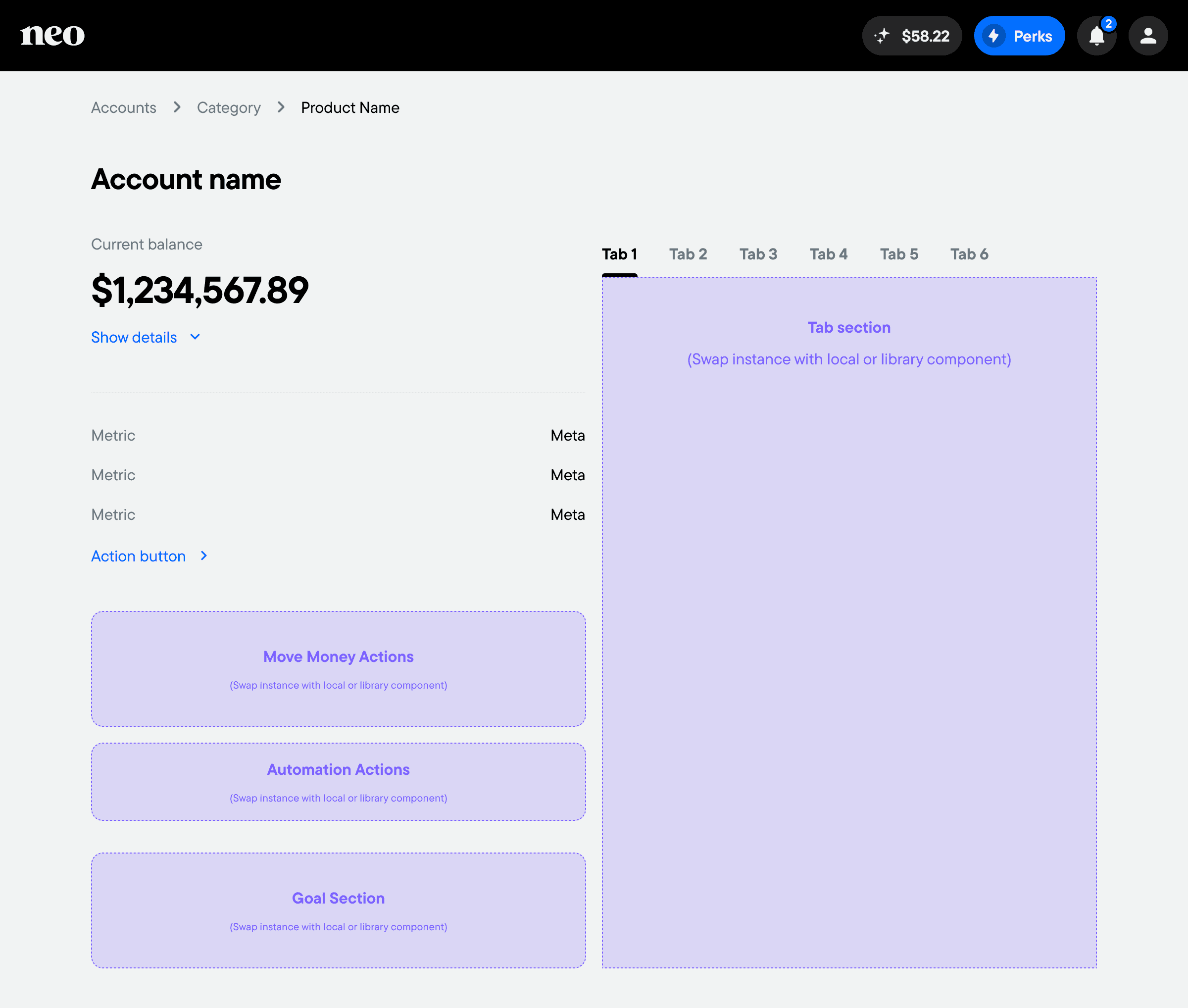

Account Details breakdown

Total balance

$123,456.789

Show details

9:41

Rainy Day Dream Vault

High-Interest Savings

Header and balance

The header & balance section helps customers quickly understand their account balance and makes it easy to dive into more complicated details when needed.

To make sure of this, we:

provide customers with the actionable account balance at the surface level.

don’t unnecessary totals at the surface level

show only account balance information in the accordion to avoid confusion.

If the data doesn't contribute to helping the customer understand how their balance is made up, it likely belongs in a different section of the page.

Components used

Secondary header

Balances accordian

Available

$3,456.78

Credit limit

$5,000.00

Utilization

24.69%

Manage credit

Health Metrics

This health metrics section houses the metrics that help customers understand the health and outlook of their account.

Typically each account type will have a specific intention. For example, a savings account is intended for saving money. Metrics like the interest rate and the interest earned to date are metrics that help customers understand how the account is performing toward that savings goal.

Often times, features and functionality will be closely tied to the account’s health metrics. The action button allows us to make these actions available directly in context to the metrics that help inform their decisions.

Components used

Health Metrics

Payment due in 15 days

Pay now

Auto-Save

Off

Move Money

Move money section facilitates moving money in, out, and around the Neo ecosystem in context to the account that’s currently being viewed.

We should ensure that users have full control and visibility over their financial movements with the ability to efficiently manage it.

Typically there are 1 or 2 move money actions that are used significantly more than the others, and we'll want to prioritize them in the experience. For example, in the Everyday Spending account, we prioritize the transferring between accounts and sending money.

Components used

Secondary header

Balances accordian

Embedding design thinking into templates

Page templates bake our design thinking right into the system. With a mix of properties and slot components, designers can quickly build pages that follow system patterns while still having full control over the content inside.

app

web

the impact

Early results and adoption

After launch, we started to see early signals that the new system was making an impact.

Customers are trusting Neo with more of their financial goals

There's been a 16% increase in customers actively using more than one account.

Customers with > 1 account (%)

Launch!

50

40

30

20

10

0

Customers are unlocking more accounts and features

The number of customers using at least one key feature — like Balance Protection — has increased from 5% to 9%.

Customers using a core feature (%)

Launch!

50

40

30

20

10

0

Neo raises $360 million in Series D funding

About three months after launch, Neo closed its largest funding round yet, raising $360 million in Series D financing.

It was a strong signal that investors believed Neo had built the foundation needed for its next stage of growth.